Please tell me I’m not alone in this. You gather all your financial documents for tax time when you look at your gross income for the year. Then the thoughts start. Is that number right? Did I really make that much money? Where did it all go? That can’t be right. With tax time just behind us, you may ultimately be left with the realization that many people have faced: “I make too much money to not be further ahead on my financial goals.”

I know those thoughts because I have had those thoughts. It turns out that the solution to the problem of my financial inefficiency is easier than I thought. The problem was not my paycheck, it was my approach to managing it. I was playing financial whack-a-mole, and it was costing me valuable time in making progress on my goals.

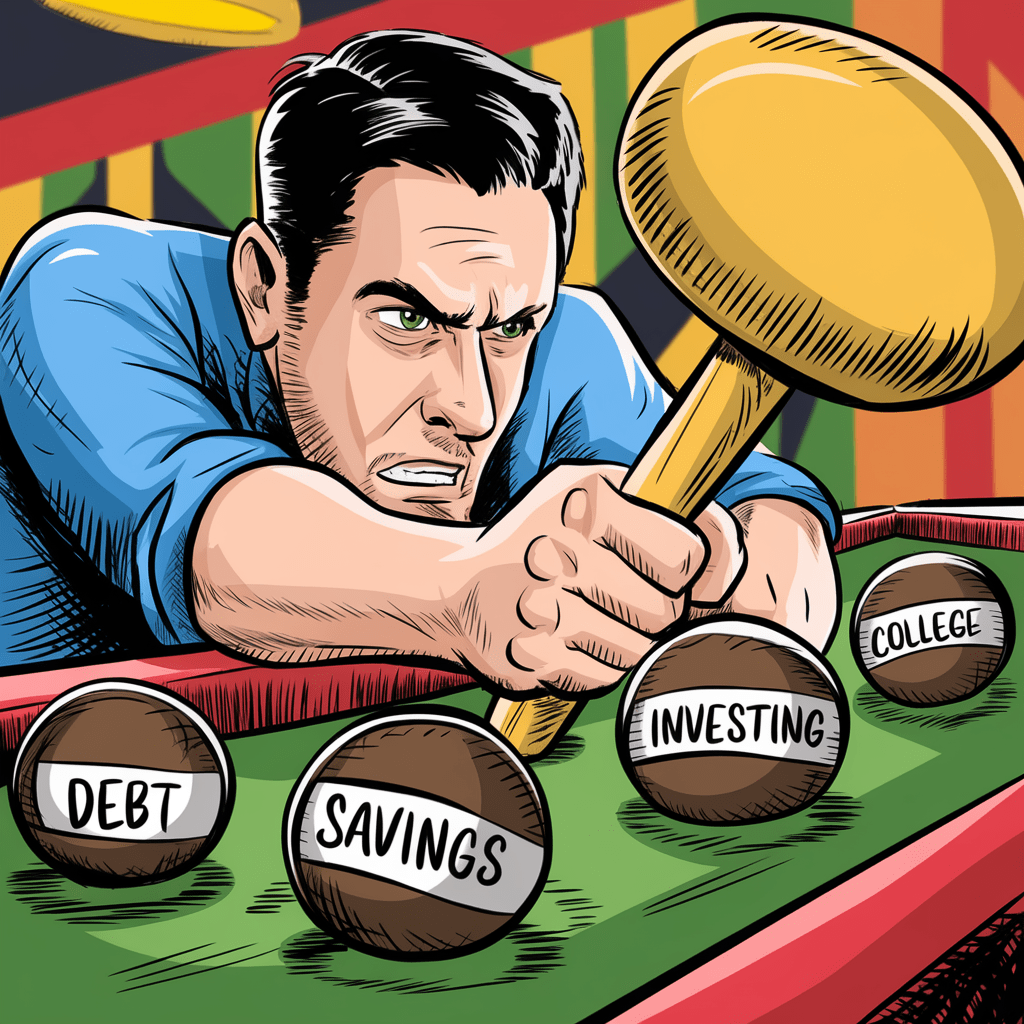

What is Financial Whack-A-Mole?

Let’s make sure every knows what Whack-A-Mole is before we build on the analogy. Whack-A-Mole is a popular arcade game commonly found at fairs and venues like Chuck E. Cheese. Players use a mallet to strike moles that randomly pop up from different holes on the game board. The challenge is to hit the moles quickly before they retreat back into their holes.

The game is chaotic, fast-paced, and often leaves you feeling like you could have done more.

The financial version of Whack-A-Mole is how people manage money when they get busy. I was one of those people. Who has time to do more than run the kids to their activities, hold down a job, make sure the bills are paid, put food on the table (or receive it through the car window as you drive through) and then do the same thing again next month? That is pretty normal, but “normal” was not getting me where I wanted to be.

Where I wanted to be was a place where money wasn’t stressful. A place of order and progress. Dave Ramsey calls it “financial peace,” and he patterned his company around showing people how to achieve it. Even without an eye-popping income, it is possible to achieve financial peace.

I was really good at playing Whack-A-Mole, but it was anything but peaceful. We had a two-income household with two kids, four schedules, and a dog. Every month it felt like some unexpected expense would pop up. An unplanned vet visit. New tires (wait, didn’t we just get new tires?) August was bad. Band fees for two schools, sports fees, dance fees, etc. Just when it felt like there was some breathing room, something would suck the air out of the room and the money out of our wallet. Thinking long term about retirement, saving for college for two kids, setting aside money for vacation, and trying to pay off our mortgage early was hard when these other expenses kept surprising us.

The Magic of Intentionality

As an experienced financial whack-a-mole player, I was trying to do too many things with my money all at once. It meant that I made tiny bits of progress, but it spread us too thin across too many goals to have good progress … or peace. Just like with the whack-a-mole game, nothing ever got fully resolved. Something was always likely to pop up and need attention. Too many things were in the balance, and it felt like I was always close to dropping a ball (or not whacking the right mole).

Enter the magic of intentionality. There are two changes that we made in our behavior that made a world of difference. First, there was the idea of planning the month in advance. I talked through each month ahead of time with my wife. What expenses did we expect? What kinds of things popped up last year at this time? What birthday gifts are we buying, what weddings are we attending, etc. to help us understand what expenses are likely next month. Those items were all baked into our budget before the start of the next month. We could apportion the money however we saw fit, but planning in advance meant fewer surprises. We also planned for date nights, saving for car insurance payments that were due, even some “fun money” to give or spend on a whim, but all these items had a plan and a budget number, and they all added up to the amount we knew would be coming in from our paychecks.

Surprises happened less often thanks to that forethought, but when they did, we knew what levers to pull to find the money. Oops, we needed to pay $500 for a repair. No problem, we would go on one fewer date night, reallocate money from a couple discretionary areas, delay another elective expense until next month and presto we “found” $500. Knowing exactly how much we set aside for each spending category allowed us to adjust our choices when unexpected expenses appeared. Doing a monthly budget was a huge help to tamp down the stress of these surprise expenses.

The second key change that brought us peace was learning to focus our efforts. Instead of trying to tackle everything at once, we chose one main priority and gave it our attention, while maintaining just enough progress in other areas. This approach reduced the number of things we had to juggle and made our financial life much more manageable. It was like permanently closing a few mole holes in the game. Focus made all the difference.

Don’t build an emergency fund, pay off debt, max out retirement, max out college savings, and pay off your mortgage, all while planning a dream vacation. You can’t have it all at once. Once I understood that, we started to focus. Do we have sufficient funds in case of an emergency? Our emergency savings were good but not great. Let’s spend a short amount of time and knock that out so we can stop dribbling money into an emergency account. In our case, we were close enough to paying off our house that we were able to be completely free of a house payment three months after we understood the power of focus. We permanently closed up that mole hole and freed up income that we could redirect to other areas. We stepped through a process to get a full emergency fund built, amp up our retirement and college savings, and start to really knock out our financial goals, all because we applied focus.

The Results of Intentionality

With a budget and a focused plan – and no change in income – the stress level plummeted, and the goals started to fall in place. Making these key changes was a process that took time to master, but it gave us much more traction on each goal as we focused on it. Some of our goals were even a little fuzzy), but now I find myself able to retire and invest my daily time outside of acquiring a paycheck. I am free to help care for our parents, travel, spend time helping friends, and work on passion projects.

For me, empowering people through personal financial education is a great way to spend my time. That’s why I right these articles – to encourage others and share wisdom that I have learned through my own life, both the successes and blunders. I know from my own experience that getting a handle on your money is the fastest path to hitting your financial goals, whatever they may be. I now fill my day with hiking, teaching, coaching, woodworking, writing, camping, spending time with family and friends. That is not a brag, but a byproduct of trading whack-a-mole for a plan. I highly recommend taking the time to be intentional with your money, and I’m happy to help anyone as they leave the whack-a-mole life behind. The power of focus is real, and using the same money more thoughtfully gave our family a lot of peace. I hope this article and others I write will give you ways to fine tune your lives to achieve peace for you and your family.

For tips on Managing Your Dollars with Common Sense, read the Loose Change blog or reach out to KJ Financial Coaching for free coaching to break out of your paycheck-to-paycheck rut. I love empowering people to find peace in their financial lives.